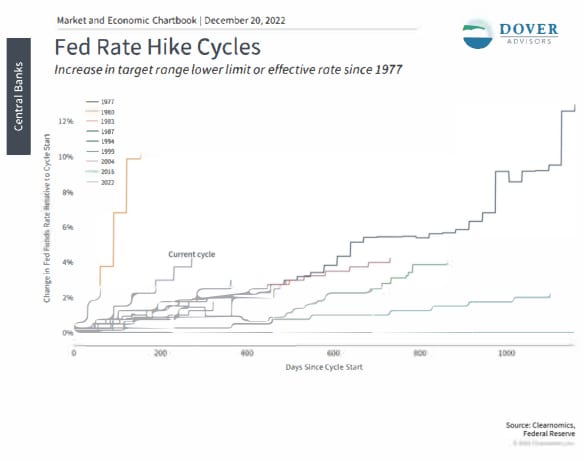

The Fed is raising rates at one of the fastest paces in history

To highlight how manic markets have been, we have only to look at the many swings in sentiment this year. Markets fell from their all-time highs at the beginning of the year due to concerns that the Fed wasn’t reacting quickly enough to inflation. Markets then rallied in March when the Fed began to raise rates, only to then plummet into bear market territory as the inflation data worsened. Markets then rallied 17% from June to August in hopes that the Fed would slow its rate hikes, for fear of a recession. These hopes were dashed when Fed Chair Powell doubled down on the inflation battle by maintaining 75 basis point hikes, causing markets to give up their gains. Markets then jumped 8% in October and 5% in November, some of the best monthly gains in history, before once again stalling out.

Markets have responded to rising inflation all year

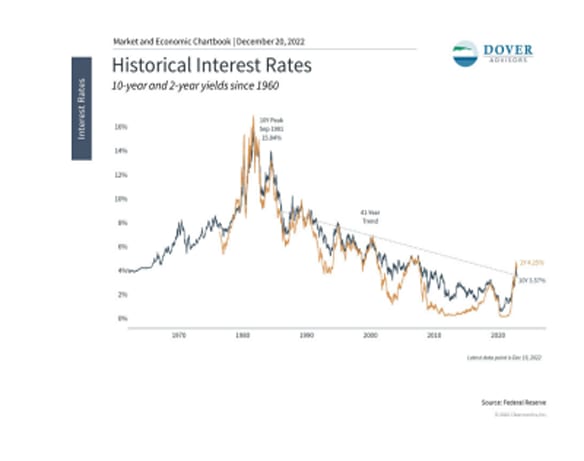

Interest rates broke a four-decade pattern

Ned Abbe

Co-CIO

Jess Ellington

Co-CIO

Important Information:

The views expressed in this commentary are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur.

The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your attorney or tax advisor.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability, or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

Risk associated with equity investing include stock values which may fluctuate in response to the activities of individual companies and general market and economic conditions.

Although bonds generally present less short-term risk and volatility risk than stocks, bonds contain interest rate risks; the risk of issuer default; issuer credit risk; liquidity risk; and inflation risk.

Dover Advisors, LLC (“Dover”) is a registered investment advisor. Advisory services are only offered to clients or prospective clients where Dover and its representatives are properly licensed or exempt from licensure. For additional information, please visit our website at https://doveradvisors.com/.